March 2005

Volume 03, Issue

10

March 2005 |

|||||

Volume 03, Issue

10 |

|||||

| Focus on Finance |

Aim at the targets (Enterprise Financial Targets) Boeing looks to drive future

growth through a

balanced approach that involves improving

revenues, earnings, cash flow and return on net assets Boeing people traditionally use Economic Profit as an important financial measure to assess how the business is faring. But as part of an evolution of the financial management of the enterprise, Boeing is moving toward a more balanced approach that involves four performance metrics, rather than just one. These metrics, collectively known as the Enterprise Financial Targets (EFT), provide a common set of financial goals that encourage everyone at Boeing to focus on increasing and sustaining value. In addition, they're measures that are commonly understood by the financial community. That lets Boeing use the same terms to talk with external and internal audiences.

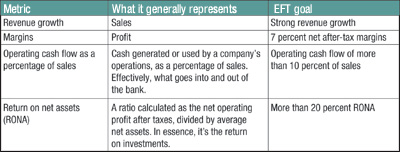

Q: What are the Enterprise Financial Targets, and why are we introducing them? A: The Enterprise Financial Targets are quantitative, company-level targets in four key areas that demonstrate what success looks like for Boeing in terms of overall financial performance. The new targets are an evolution of the disciplined approach we already have to running our business today, and they provide a balanced approach for how we'll grow it tomorrow. They're intended to ensure we have absolute focus on what we need to do to drive behavior that results in sustained value creation through top shareholder returns. By looking at four metrics, we get a balanced approach to financial management of the enterprise and achieve consistency between the way we track, assess and communicate our financial performance to all stakeholders. Wall Street and investors understand the four elements very well, unlike Economic Profit (EP), which was solely an internal metric Boeing used that few outside the company understood. Q: What are the four metrics? A: The four metrics are revenue growth, net margin, operating cash flow as a percentage of sales, and return on net assets (RONA). Specifically, over the long-term, Boeing wants to achieve

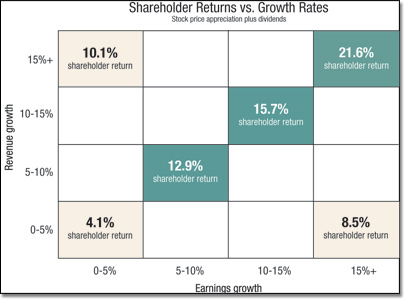

A: In mid-2004, Boeing's Finance team analyzed companies in our and other industries to see what characteristics top-performing companies shared. If you look at historic performance of top performers, you see that balanced revenue and earnings growth is a very important factor in creating value and increasing returns to shareholders. Analysis shows the market most rewards companies that consistently achieve growth in both revenue and earnings, rather than favoring one at the expense of the other. Similarly, cash flow is a very important aspect of measuring the financial health of a business, as is the allencompassing measurement RONA, which incorporates asset utilization with profit (also partially driven by revenue). Since what gets measured usually gets achieved, establishing firm targets in these four areas provides a framework for guiding strategic decisions about how we run the business for success. Q: Can you give some real-world examples of each metric and how employees can affect them? A: Let's start with revenue. An easy way to think about it is, the more airplanes you deliver, the more revenue you're going to get. So generally, as Boeing sells more airplanes year-over-year, its revenue will grow. In terms of margins, a good real-world example is all the effort going into our Lean Enterprise Initiative, including looking at facility utilization, more efficient processes, the moving line concept, etc. These actions reduce costs and therefore increase margins. In terms of cash, cash is strongly related to earnings. Ultimately, cash and earnings will equal each other. But generally there is a timing difference. For example, the time that it takes for Boeing to actually collect dollars from a customer versus when it recognizes the sale and profit upon delivery—that timing is the difference between earnings and cash in the bank. When we negotiate better terms with our customers and suppliers in terms of collecting and disbursing cash, we can improve cash flow. RONA encompasses revenue, earnings and cash flow. Examples of RONA improvement are

These items reduce the amount of cash that the company needs to have tied up in assets such as inventory, facilities, equipment or receivables. This generates additional cash flow, which is then available to reduce borrowing or increase returns to stockholders.

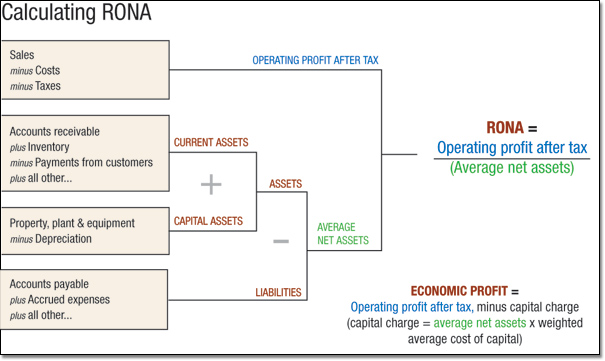

A: Because balanced financial performance is what will drive sustained value creation and is what the market rewards. By looking at four different measurements, the Enterprise Financial Targets represent a balanced approach to managing the financial performance of The Boeing Company. The challenge for us is that we are in a cyclical industry, so there may be years when revenue comes down. The key is to drive revenue growth over the longer term. During "down" revenue years, the company will need to focus even more on the other metrics and demonstrate performance in these areas. Q: How do Economic Profit and RONA differ? A: RONA and EP measure the same things. RONA is a ratio. It divides the operating profit after tax by the net assets of the corporation. But EP is an absolute dollar amount, not a percentage. It is calculated by subtracting from the operating profit after tax a capital charge associated with the net assets. The capital charge is a measurement that essentially takes your net assets and applies a weighted average cost of capital to them that represents the cost of holding the assets of the business. The net assets used in EP are the same net assets used in the RONA calculation. Q: If RONA and Economic Profit are similar and measure similar things, why are we changing to RONA? A: Adopting RONA will move us to a more traditional and widely used measurement of return on investment. EP is not widely used outside of Boeing. When we look at benchmarking Boeing against other companies in the aerospace industry and beyond—especially the top-performing companies Boeing wants to emulate—we need to use a measurement that lets us compare ourselves meaningfully. You've probably heard Boeing leadership say our goal is to have financial performance in the top 25 percent, or the top quartile, of companies listed on the S&P 500 (an index of 500 widely held stocks). Using RONA provides a basis for comparison and a way to communicate externally with a known metric. If we are going to use it externally, we felt it was prudent to also use the same measurement internally so that we're talking the same language. Based on the ability to benchmark RONA, we can set a long-term target for RONA (that is part of the balanced financial metrics to drive sustained value creation), which we can't easily do with EP. Q: Can we improve RONA the same way we worked to improve EP? A: Yes, absolutely. And that's important to recognize: The behaviors that we're currently driving are not expected to change. Things we've been doing—like focusing on execution, improving product quality, reducing cycle time, negotiating good deals with customers—all of those activities will continue to drive better performance. Q: Are any of our aerospace peers among those top-performing companies? A: This depends on what period you measure and as of what date. As of December 2004, United Technologies and General Dynamics were both in the top quartile for the 10-year return period. General Dynamics, Northrop Grumman and Lockheed were in the top quartile for the five-year period. United Technologies, again, for the past three years. Raytheon for the

past one year.

As of December 2004, Boeing was not

among the top quartile for the Q: What's the impact to things like the Employee Incentive Plan (EIP), ShareValue Trust or other incentive compensation? A: Again, the targets are set in order to drive long-term value creation, and that value is expressed in terms of stock price. Incentive compensation initiatives that are tied directly to stock price (including Share-Value Trust and Executive Performance Shares), therefore, stand to benefit from top-quartile performance and subsequent stock appreciation. EIP and Executive Incentive Compensation, although not directly related to stock price, benefit from the focus on execution and balanced performance driven by EFT. Starting in 2006, we expect to use RONA instead of EP as the metric to determine EIP and Executive Incentive Compensation. Q: Do we need to make acquisitions to achieve "strong revenue growth"? A: Top shareholder return companies, even cyclical ones, demonstrate strong revenue growth over time. The actual growth rates vary, but for many it is in the double-digit range. In terms of acquisitions, we don't necessarily need to do them right away. Given our current market position and our backlog, to the extent that we execute our current business, we will grow in the near term with the portfolio we have now. Over the longer term, the company will continue to pursue value-creating acquisitions that fit with our strategy. If we want long-term growth, we need to invest to get there—whether those investments are in acquisitions or in new products. It's important to note that Boeing's growth rate in recent history has largely been generated through acquisitions. But in the near term, with the pending commercial up-cycle, we expect to grow with the portfolio we have now. Q: How does achieving the EFTs benefit employees? A: Financially successful companies are able to offer better compensation, more jobs and better opportunities for career growth. The more successful Boeing is at achieving top financial performance as measured by EFT, the more the company will grow and the more opportunities will be created for all Boeing people.

|

| Contact Us | Site Map| Site Terms | Privacy | Copyright | ||||||

| Copyright© Boeing. All rights reserved. |

To explain what the EFTs are and further explain why Boeing is using

them,

Boeing Frontiers spoke to James Bell,

chief financial officer.

To explain what the EFTs are and further explain why Boeing is using

them,

Boeing Frontiers spoke to James Bell,

chief financial officer. Q: How were these metrics

chosen?

Q: How were these metrics

chosen?