|

||||||||

| Focus on Finance |

| Goodwill hunting How an accounting rule obscured Boeing's strong first-quarter performance BY JUNU KIM Boeing on April 23 reported a first-quarter loss of $478 million. Yet the company also said the underlying performance of the company's aerospace businesses was strong. These seemingly paradoxical statements stem in large part from a noncash charge of $913 million due to the impairment of goodwill. It is important to note that this type of charge has no effect on current-period cash flow or the day-to-day operations of the company. These noncash charges can obscure the fact that Boeing continues to perform well. "The reported net loss figure doesn't accurately reflect the quality of our operating performance, which remains strong," said Mike Sears, Boeing Chief Financial Officer. The first-quarter results raise the question: What is goodwill? When a company purchases another firm, it determines the price it's willing to pay. It must also determine the "fair value" of the identifiable net assets being acquired. This includes both tangible assets (land, machinery, etc.) and intangible assets (trademarks, customer relationships, patents, etc.), offset by assumed liabilities (accounts payable, debt, etc.). The difference between the amount paid for a company and the fair value of its net assets represents goodwill, which is accounted for as an asset on the acquiring company's balance sheet. Most acquisitions cause the buying company to put goodwill on its balance sheet. Why would a company pay more than the "fair value" of the net assets? Just as most homebuyers would be more interested in buying an existing, standing residence—than in buying a house's separate components (lumber, windows, etc.)—the amount paid to purchase a company can include a premium above the value of the "parts" that reflects the value of buying a "complete package." "Some media personnel characterize goodwill as the amount one company 'overpaid' to acquire another," said Cheryl Bayer, World Headquarters manager of Accounting Policy. "Most corporate development and accounting experts, however, believe it represents synergies and opportunities that the acquiring company expects to realize as a result of the acquisition."

The way Boeing now tests for goodwill impairment is consistent with accounting rules that became effective Jan. 1, 2002, for Boeing. The new rules require a comparison of the book value of goodwill to the fair value of goodwill—estimated by Boeing using discounted future cash flows—instead of the acquired business's undiscounted future cash flows, which are naturally higher than discounted cash flows. Accordingly, the new rules made goodwill impairment testing more rigid—and caused many companies, including Boeing, to record goodwill impairments for the first time in their history. The new rules also require companies to test their goodwill for impairment once a year and when an event occurs that indicates a possible impairment exists. Boeing has selected April 1 as its annual testing date.

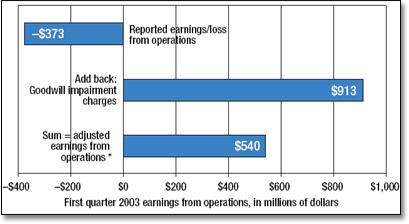

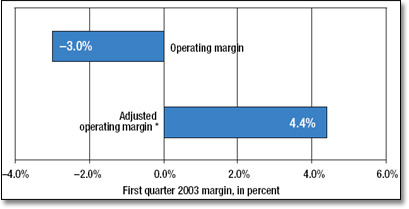

Boeing's first-quarter adjusted earnings from operations—which as defined by the company excludes the noncash charges for goodwill impairment and which Boeing management believes provides an important perspective on the current underlying operating performance of the business—shows that the company continued to run profitably, despite the challenges in its commercial markets. For the quarter, Boeing reported a loss from operations of $373 million and an operating margin of minus 3 percent. Excluding the noncash goodwill impairment charges, Boeing recorded $540 million in adjusted earnings from operations and an adjusted operating margin of 4.4 percent. Those figures reflect strong revenue growth in defense programs and production efficiencies at Commercial Airplanes (see chart). "Overall, our businesses are running well," Sears said. "Commercial Airplanes continues to operate profitably in a significantly depressed market, and our Integrated Defense Systems business continues to perform well in strong markets. Boeing remains positioned for profitable, long-term growth." * Represents a non-GAAP (Generally Accepted Accounting Principles) measure. Boeing does not intend for the information to be considered in isolation or as a substitute for the related GAAP measures. Other companies may define the measures differently.

|

| Contact Us | Site Map| Site Terms | Privacy | Copyright | ||||||

| © 2003 The Boeing Company. All rights reserved. |

Impairment of goodwill represents a reduction in the value of the acquired

business, business,

driven principally by its estimated

future contributions to financial performance

of the combined company. The impairment

analysis is primarily driven by estimated

future contributions to the combined company's

value creation, and the company's stock price as of the analysis date. And it

is interesting to note that impairment of goodwill is a one-way event; if the

acquisition's estimated

future contributions to value and/or

the company's stock improve after the analysis, the company is not allowed to

reverse the impairment charges or write the goodwill back up to its pre-impairment

level.

Impairment of goodwill represents a reduction in the value of the acquired

business, business,

driven principally by its estimated

future contributions to financial performance

of the combined company. The impairment

analysis is primarily driven by estimated

future contributions to the combined company's

value creation, and the company's stock price as of the analysis date. And it

is interesting to note that impairment of goodwill is a one-way event; if the

acquisition's estimated

future contributions to value and/or

the company's stock improve after the analysis, the company is not allowed to

reverse the impairment charges or write the goodwill back up to its pre-impairment

level.  A company that recognizes goodwill impairment must report the amount

as a

reduction to its reported income for the period. As a result, the $913

million for goodwill impairment

appeared on Boeing's

first-quarter financial results as

a negative item.

A company that recognizes goodwill impairment must report the amount

as a

reduction to its reported income for the period. As a result, the $913

million for goodwill impairment

appeared on Boeing's

first-quarter financial results as

a negative item.